All Categories

Featured

Table of Contents

The main differences between a term life insurance policy policy and an irreversible insurance plan (such as entire life or global life insurance policy) are the duration of the plan, the buildup of a cash money value, and the cost. The ideal option for you will depend upon your needs. Right here are some things to think about.

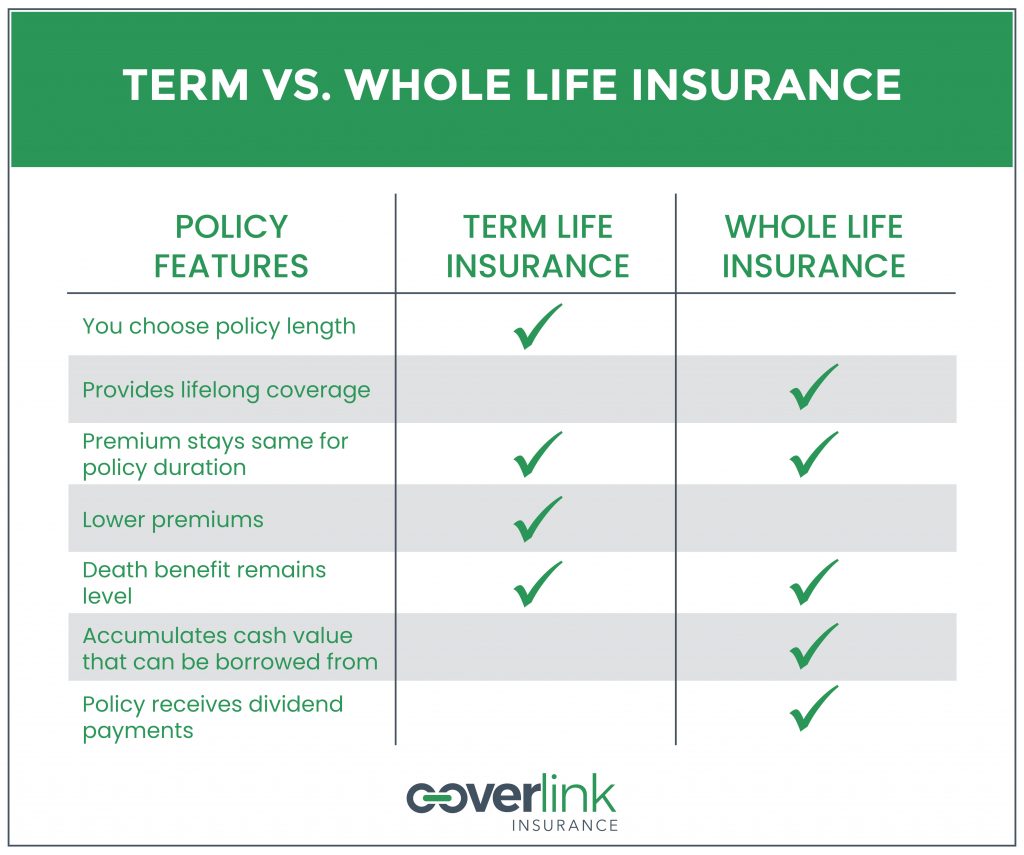

People who possess whole life insurance policy pay extra in costs for much less protection but have the safety of understanding they are safeguarded forever. Level death benefit term life insurance. Individuals that acquire term life pay costs for a prolonged period, but they obtain absolutely nothing in return unless they have the tragedy to die before the term runs out

The performance of permanent insurance can be steady and it is tax-advantaged, supplying added advantages when the supply market is unstable. There is no one-size-fits-all solution to the term versus long-term insurance policy dispute.

The rider assures the right to convert an in-force term policyor one ready to expireto a long-term plan without experiencing underwriting or showing insurability. The conversion rider ought to enable you to convert to any type of irreversible plan the insurer offers without limitations. The main functions of the biker are keeping the original wellness score of the term plan upon conversion (also if you later on have wellness concerns or become uninsurable) and choosing when and just how much of the coverage to transform.

Who offers Level Term Life Insurance For Seniors?

Of training course, total costs will certainly raise dramatically given that entire life insurance policy is extra costly than term life insurance - Level term life insurance calculator. Clinical problems that create during the term life duration can not trigger premiums to be increased.

Entire life insurance policy comes with substantially greater month-to-month costs. It is indicated to supply insurance coverage for as long as you live.

It depends upon their age. Insurance provider established an optimum age limit for term life insurance policy plans. This is usually 80 to 90 years of ages, but may be higher or reduced depending upon the company. The costs also increases with age, so an individual aged 60 or 70 will pay significantly greater than someone years younger.

Term life is rather comparable to cars and truck insurance coverage. It's statistically unlikely that you'll need it, and the premiums are cash away if you do not. Yet if the worst takes place, your family will obtain the benefits.

Who are the cheapest Level Term Life Insurance providers?

___ Aon Insurance Coverage Services is the brand name for the broker agent and program management operations of Fondness Insurance policy Providers, Inc. (TX 13695) (AR 100106022); in CA & MN, AIS Fondness Insurance Policy Firm, Inc. (CA 0795465); in OK, AIS Fondness Insurance Policy Services Inc.; in CA, Aon Fondness Insurance Policy Solutions, Inc.

The Strategy Agent of the AICPA Insurance Trust, Aon Insurance Policy Services, is not associated with Prudential. Group Insurance policy protection is issued by The Prudential Insurance Coverage Firm of America, a Prudential Financial company, Newark, NJ.

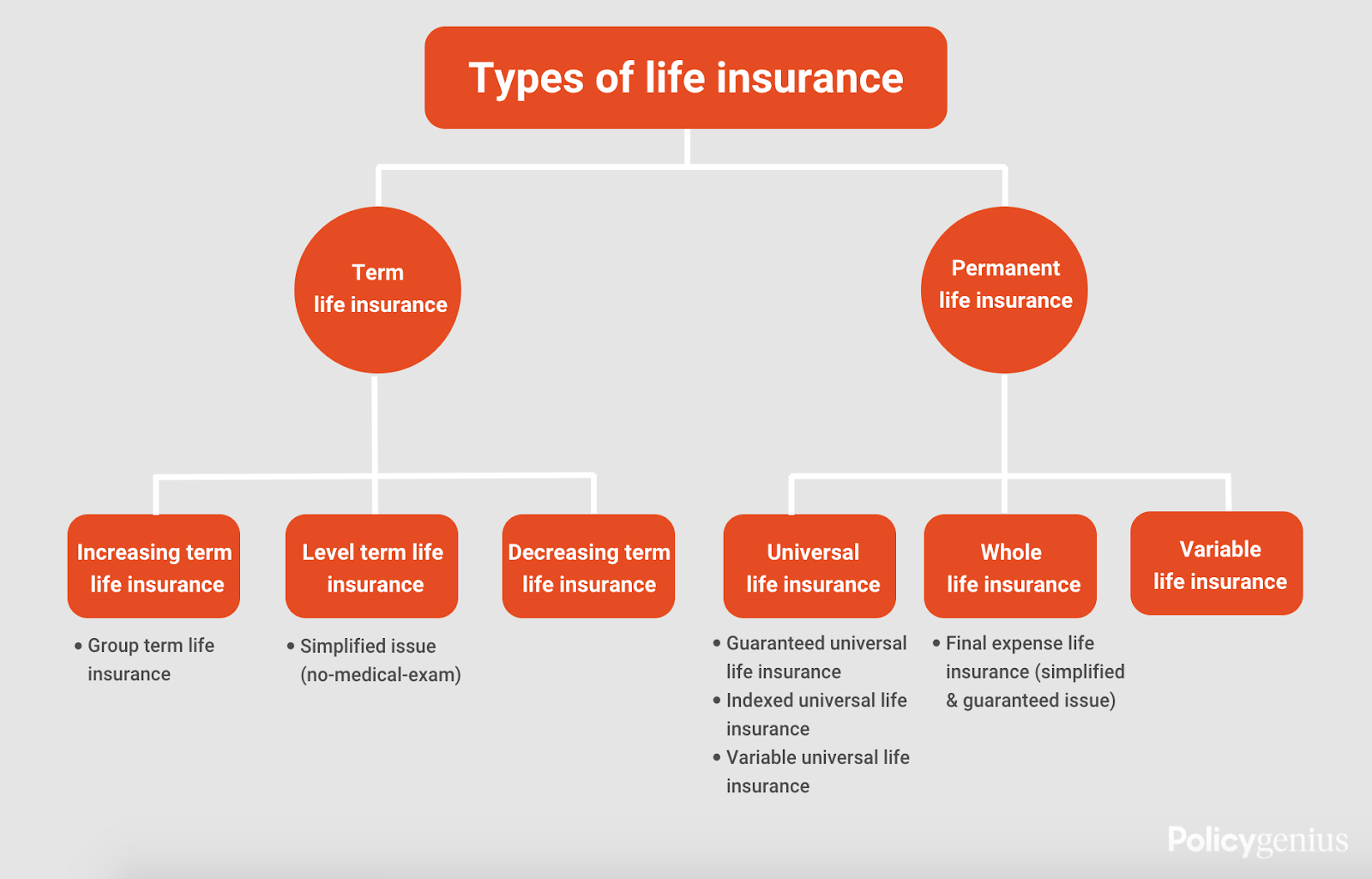

For the most part, there are two kinds of life insurance policy plans - either term or irreversible strategies or some mix of both. Life insurance firms supply numerous types of term plans and traditional life plans along with "interest sensitive" products which have ended up being extra common because the 1980's.

Term insurance policy supplies defense for a given time period - Affordable level term life insurance. This period can be as brief as one year or offer insurance coverage for a certain number of years such as 5, 10, twenty years or to a specified age such as 80 or in some situations up to the earliest age in the life insurance policy mortality

How do I apply for Level Term Life Insurance For Seniors?

Presently term insurance policy prices are extremely competitive and among the lowest historically seasoned. It needs to be kept in mind that it is a widely held belief that term insurance coverage is the least expensive pure life insurance policy coverage readily available. One needs to assess the policy terms very carefully to determine which term life choices appropriate to fulfill your specific conditions.

With each new term the premium is increased. The right to restore the plan without proof of insurability is an essential advantage to you. Otherwise, the danger you take is that your health might deteriorate and you may be not able to obtain a plan at the exact same prices and even in any way, leaving you and your recipients without insurance coverage.

The length of the conversion period will vary depending on the kind of term plan bought. The premium price you pay on conversion is usually based on your "present obtained age", which is your age on the conversion day.

How do I apply for Level Term Life Insurance Coverage?

Under a level term policy the face quantity of the policy continues to be the very same for the whole duration. Usually such plans are marketed as home mortgage defense with the quantity of insurance coverage lowering as the balance of the home mortgage reduces.

Commonly, insurance companies have not had the right to alter costs after the plan is offered. Considering that such policies may continue for years, insurance providers have to use traditional death, rate of interest and expense price price quotes in the costs estimation. Flexible premium insurance, nonetheless, enables insurance firms to offer insurance at reduced "present" costs based upon much less traditional presumptions with the right to transform these costs in the future.

While term insurance is designed to give protection for a defined time duration, irreversible insurance is designed to give coverage for your entire life time. To maintain the costs rate level, the premium at the younger ages surpasses the real price of security. This extra premium constructs a get (cash money worth) which assists pay for the policy in later years as the cost of defense increases over the costs.

What is 30-year Level Term Life Insurance?

With degree term insurance, the cost of the insurance will certainly stay the exact same (or possibly decrease if rewards are paid) over the regard to your policy, usually 10 or twenty years. Unlike long-term life insurance policy, which never runs out as lengthy as you pay premiums, a level term life insurance plan will certainly finish eventually in the future, normally at the end of the duration of your level term.

Due to this, many individuals make use of long-term insurance as a steady financial planning tool that can serve several demands. You may be able to transform some, or all, of your term insurance coverage during a set period, normally the first ten years of your policy, without requiring to re-qualify for coverage even if your health and wellness has actually transformed.

20-year Level Term Life Insurance

As it does, you may desire to add to your insurance protection in the future. When you first get insurance policy, you might have little savings and a big home loan. At some point, your savings will certainly grow and your mortgage will diminish. As this happens, you might wish to at some point lower your death benefit or take into consideration transforming your term insurance policy to a long-term policy.

As long as you pay your premiums, you can relax easy understanding that your enjoyed ones will certainly get a survivor benefit if you pass away throughout the term. Several term plans permit you the capability to convert to irreversible insurance without needing to take an additional health test. This can allow you to benefit from the fringe benefits of a permanent policy.

{kind=link}

Latest Posts

Instant Permanent Life Insurance Quotes

Funeral Covers

Funeral Cover